~10 min Read

Why China Is Winning the Rare Earth Minerals War

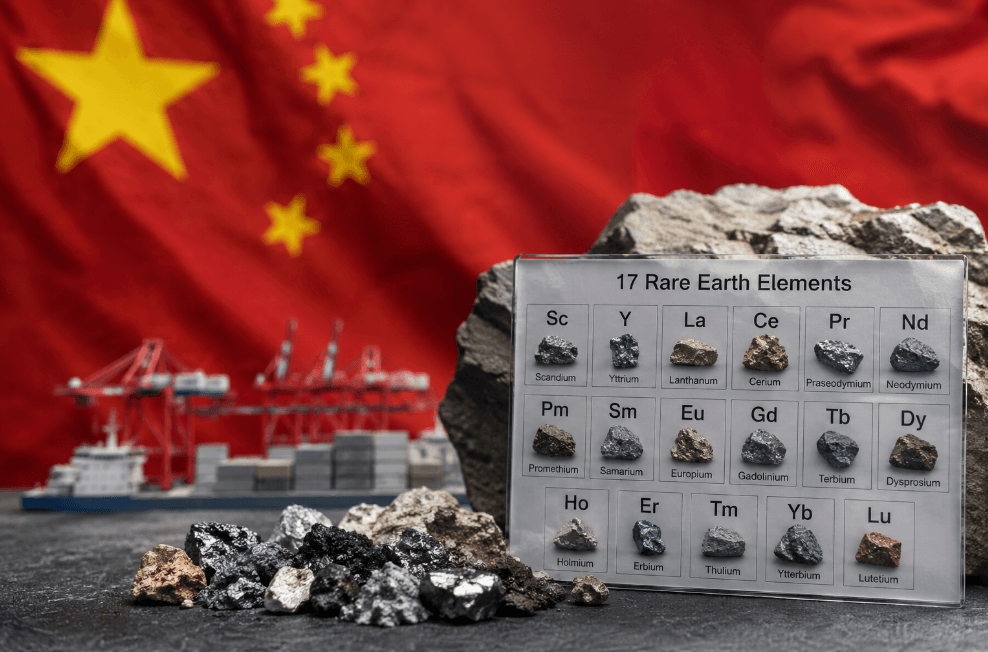

An entire battlefield is being fought with no guns, and not one soldier has fired a weapon or launched an airplane — just 17 elements (from the periodic table). China has a complete hold on this division of the elemental spectrum, to the extent that even the US military can’t construct its fighter aircraft without obtaining permission from China.

01 — The Foundation

What Exactly Are We Fighting Over?

Rare earth elements (REEs) are a set of 17 metallic elements that most people have never heard of — yet they are embedded in almost every piece of technology that defines modern life. They’re in your smartphone’s vibration motor, the electric motor of your Tesla, the guidance system of a Tomahawk missile, and the magnets inside every wind turbine spinning in the North Sea.

Here’s the paradox: they aren’t actually rare. They exist across the globe in generous geological deposits. But extracting, processing, and refining them is a notoriously dirty, chemically complex, and economically punishing process — one that most countries quietly decided wasn’t worth the trouble. China decided otherwise.

| Symbol | Element | Main Uses |

|---|

| Nd | Neodymium | EV motors, wind turbines |

| Dy | Dysprosium | High-temp magnets, defence |

| Tb | Terbium | Sonar, defence systems |

| Pr | Praseodymium | Aircraft engines, lasers |

| In | Indium | Touchscreens, semiconductors |

⚠ Defence Vulnerability

A single F-35 fighter or JF-17 jet contains hundreds of pounds of rare-earth materials. Every missile, radar system, satellite, and secure communications array depends on these elements — and currently there are no viable substitutes at scale.

| Statistic | Details |

|---|

| 90% | Global rare earth minerals processing controlled by China (IEA, 2025) |

| 70% | US rare earth compound imports from China (2020–2023) |

| $57B | China’s critical mineral investment (2000–2021) |

| 12 | Active rare earth minerals projects in the US vs 89 in Australia |

02 — The Strategy

How Did China Build a Monopoly the World Didn’t Notice?

This was a process that took many years to develop and did not just occur by chance. Whereas the Chinese government considers the rare earths to be of strategic value, rare earths have traditionally been considered to be a tradable or transported commodity by many Western policymakers, and it is likely that they did not fully understand the distinction until almost too late.

China has spent an estimated 57 billion dollars between 2000 and 2021 on developing critical materials. While mining companies in the West divert their resources towards extracting iron and gold, state-owned enterprises in China have been building the world’s most sophisticated rare-earth processing plants – rare-earth separation plants, metallizing plants, magnetic material lines, and precision engineering capabilities that convert raw ore into the essential parts that go into modern manufacturing.

“China’s strength goes far beyond mineral separation. It also dominates metal refining, magnet production, and a rapidly advancing AI-driven industrial system — capabilities that many democratic nations may struggle to recreate quickly due to political and economic constraints.”

— Fitch Ratings / BMI Analysis, May 2026

One of the steps for success was vertical integration. China has not only taken control of the mining process. It now controls the entire value chain — from the dirt in the ground to the finished neodymium magnet; as a result, any efforts to bypass any segment of the Chinese supply chain essentially become futile. For example, you may be able to mine in Australia, but without any Chinese separation capability, you only have expensive dirt and no rare earth oxides.

The second major pillar is a Technology-Economic Linkage Model that facilitates a close relationship between universities, governmental laboratories, and industry that is capable of translating knowledge-based academics into production very quickly. While the West has excelled in academia, China has successfully applied its academic work to create an industrial base that dominates the world.

03 — The Weapon Unsheathed

The 2025 Export Control Escalation — A Turning Point

For years, China’s rare earth dominance was theoretical leverage. In 2025, Beijing converted theory into practice — and the world finally understood what it had sleep-walked into.

China announces a ban on rare earth minerals extraction and separation technologies — preventing other nations from acquiring the knowledge to replicate its processing capabilities.

Indium — critical for touchscreens and semiconductor manufacturing — placed under export licensing requirements.

In direct retaliation for

Trump’s tariff announcements, Beijing restricts exports of seven heavy rare earth elements. Global markets react with immediate price spikes.

US–China talks in Switzerland produce a 90-day tariff truce. China agrees to restore rare earth minerals access — but stability proves short-lived.

China expands controls to five additional rare earth elements and restricts access to processing technology and technical expertise — a move to lock down the entire knowledge supply chain globally.

As per China’s Ministry of Commerce Announcement No. 61, effective 1 December, export controls on rare earths and permanent magnets are being imposed at the most stringent level thus far. For the first time, China plans to use the Foreign Direct Product Rule — a measure previously associated with the United States — as part of its new export control strategy.

President Trump and Chinese President Xi Jinping had a summit meeting; subsequently, the White House has been trying to negotiate what is called a general license that allows US companies to conduct business with China, and China agreed to provide the license, but it will only be valid for three years (i.e., it will expire in October 2026). Thus, right now the clocks are ticking against three years from now.

This sequence reveals an insight that is not to be found in any one of the individual actions. Rather, it shows how the actions taken show an overall design and architecture that China is now creating for Western manufacturers to be completely dependent upon the discretionary power of the Chinese government. Each time one of these actions is undertaken, the level of control increases, and whenever one of these actions has required some type of diplomatic reprieve, time is purchased, but the basic fundamentals do not change.

💡 The Game Theory Angle

Analysts at Resources for the Future contend that the Chinese government does not intend to remove its suppliers permanently through export controls but rather to employ these as tools of leverage — or a Pressure Tactic — to get concessions during negotiations with no clear indication of how long they will continue to restrict supplies. They also assert this strategy has precedent in Japan, where in 2010 the Japanese barely reduced their exports to China even though prices increased dramatically, causing the Japanese to diversify their supply chain from China over a period of ten years. The “weapon” here is the threat itself.

04 — The Real Gap

Why Western Diversification Is Harder Than It Sounds

The governments of the Western hemisphere consider obtaining rare earth minerals independence to be a priority in terms of national security. There are numerous news releases regarding these announcements. Funding is being generated via multiple mechanisms. China is still processing almost 90% of all global rare earths as of May 2026 (a number that has not changed in many years due to multiple indicated commitments).

There are reasons for this failure that are understood to represent structural deficiencies and cannot be corrected solely by the infusion of cash in a sustainable way or quickly.

The Processing Bottleneck

The most overlooked aspect of the issue is that mining is the visible component, while processing is where China’s monopoly really exists. Rare earths are mined from all over the world, but the supply chain is highly concentrated in the processing phase, as indicated by the

IEA. In the first quarter of 2026, Lynas Rare Earths — Australia’s hero and the only non-Chinese firm refining heavy rare earths — only processed eight tonnes of dysprosium and terbium (both together), whereas the international market for these elements requires thousands of tonnes every year.

The Technology Lock-In

China’s Export/Import Ban on processing technology (Effective 12/2023) has allowed China to not only control supply through restricting exports but also to block competitors from gaining access to the technical knowledge necessary to duplicate China’s manufacturing capability. All new processing plants need to be built from the ground up and require starting from a scientific principles view, combined with no existing knowledge base within other nations to support the new plants’ construction.

Japan’s Warning

Japan has been trying for over a decade to cut its reliance on rare earth metals after an incident in 2010 when China restricted exports of these materials. A decade later, in 2026, China remains the largest supplier of rare earths to Japan, having provided approximately 76% of Japan’s rare earths at that time. Even though Japan invested considerable amounts of time and resources into diminishing dependence on China, and despite having substantial industrial capacity, Japan remained approximately 75% dependent on China for rare earths. The US and Europe hope to do better than what Japan has achieved in an even shorter time frame, while facing a more fragmented manufacturing sector.

The Permitting and Time Problem

One of the greatest obstacles facing new processing facilities is the permitting and construction timeline in Western-style democracies. In addition to permitting issues, building the necessary workforce to operate facilities takes time, as workers need to be trained.

In addition, it can take years to build the supply chains necessary to support the production of rare earths in the US. One example of these efforts is MP Materials’ ongoing expansion in California and Texas.

Another example is Energies Fuels’ pilot production facility in Utah, which produced its first dysprosium in October 2025. Unfortunately, worldwide demand for rare earths continues to increase at a rate of approximately 25% per year. Therefore, the math does not favour these industries.

⚠ Defence Emergency

US munitions stockpiles were significantly drawn down following conflicts in 2025–2026. Much of the technology used in key munitions depends on heavy rare earths with few viable substitutes. The US may not have enough time before the October 2026 general license expires to build meaningful alternative supply.

05 — The Global Chessboard

China Isn’t Just Defending — It’s Expanding

While Western countries continue their discussions to develop multiple methods of governing rare earth minerals production, China is quietly obtaining more and more control over existing rare earth resources – even those located outside of its borders. Most of the media concerning this development has either not reported it or has not emphasized the gravity of this continuing action.

State-affiliated companies in China, such as Shenghe Resources, have extended Jiacheng Mining, one of their subsidiaries, into Madagascar, where new and competitive access to rare earth elements is being established. Two companies, Xiamen Tungsten and Chifeng Jilong, have developed joint-venture operations for both mining and processing operations in Laos, which contains exceptionally large deposits of heavy rare earth elements. Heavy rare earths are currently being produced in Kachin State, Myanmar, in an area that has a large rebel presence and is very geopolitically unstable, and Kachin is now the largest producer of heavy rare earths in the world, with China being the only country that currently produces any rare earths in the Myanmar Kachin region.

China’s plan is not just to maintain its position as the only producer of rare earths to China, but also to develop processing capabilities for every viable deposit of rare earths, irrespective of where the deposit is located. Thus, regardless of where any rare earths are mined, the refining will take place in China, the production of magnets will take place in China, and the country will maintain its leverage in the global rare earth minerals market.

🌏 The Australian Counter-Play

Australia is the best option to supplement Western supply chains. In 2025, it received $64 million, which represents 45% of worldwide rare earth minerals exploration investments, and there are still 89 potential projects active today. In May 2025, Lynas produced commercial amounts of dysprosium oxide for the first time from outside of China and signed a US-Australian Critical Minerals Framework in October of that year. Iluka Resources received a $1.25 billion loan backed by the government to build a new refinery. While progress is being made, the relative size of progress compared to China’s industrial scale is still small.

06 — The Path Forward

What Would It Actually Take to Break China’s Hold?

According to Fitch Ratings and most independent analysts, China is projected to hold between 80% and 90% of the world’s rare earth processing market share through 2030 at current trajectories. It’s not a matter of pessimism; it is arithmetic based on construction timelines, investment flows, and the priceless value of cumulative expertise.

There was $6.3 billion of announced investments in 2025 in rare earth minerals projects outside of China, of which 60% was from US government sources. Another $2.8 billion from outside China was announced in Q1 2026 alone. Neither amount is inconsequential, but neither is sufficient to replicate in a few years what took China 40 years to build.

There are three items that would materially shift the balance. First, commercial-scale independent midstream processing capabilities — not pilot operations generating kilograms, but refineries generating thousands of tons. Second, true allied supply chain coordination — the US–Australia framework, the US–Japan critical minerals partnership announced in October 2025, and a March 2026 deep-sea mining memorandum of cooperation are all good starts but are still in the beginning stages. Finally, technological substitution — designing advanced systems that do not utilize or utilize very few elements that are in significant control of China. This will require a long-term research effort, not an immediate fix.

⏱ The Clock is Ticking

The general export licence from China for US companies will expire in October 2026, at which time, unless the current geopolitical situation changes, there is a risk of acute supply disruptions for materials that cannot be relocated to other markets. Options to create alternate sources of supply are rapidly diminishing while the infrastructure needed to develop them is still under construction.

Final Assessment

China Is Winning. But the War Is Not Over.

The domination of rare earth element processing in China has its roots in geopolitical intent rather than an accident of geopolitics. For the past forty years, China has implemented a deliberate, methodical, government-directed strategy of investment in infrastructure (over $57 billion) that Western governments believed at some time would be either too dirty or marginal to bother to develop. By the time Western policymakers in Washington, Brussels, and Tokyo appreciated the strategic implications, the supply chain was established, the expertise was in place, and the advantage was legitimate.

The 2025 export controls transformed a theoretical vulnerability into a functioning crisis. The time allowance provided by the diplomatic reprieves did not change anything fundamentally. As of May 2026, while the West is constructing a base, it is doing so against a background of almost total reliance on China and competing with a timer created by Beijing, not Washington.

China is winning the war for rare earth metals. The question is not whether the West can eventually catch up with China — it most likely will, but it will take a decade or more to do so. The real issue is whether or not the West can accomplish this quickly enough to keep Beijing from using its advantage to redefine the rules for global technology, defence, and trade until then. The answer to that question is currently being generated very dangerously.