Is the U.S. Dollar Losing Its Dominance – How is the US Dollar in Trouble?

Maybe you are also noticing in the current global power shifts that the US dollar is in trouble and its dominance is decreasing shows data, but how? You will get all your answers in this Blog of Brainification.

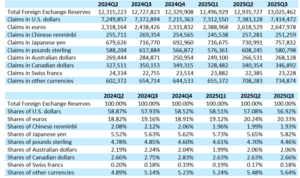

According to the reports of the Federal Reserve System and IMF data of Quarter 3, by the end of 2025, global foreign exchange reserves had risen to approximately $13 trillion from $12.94 trillion, of which the U.S. dollar remained the leading component, making up about ≈56.92%, ≈20.43% Euros,≈5.82% Japanese Yen (JPY), and Chinese renminbi 1.93% decreased from ≈1.99%-2% in the previous quarter.

America’s Growing Debt and Its Impact on the US Dollar Trust:

On New York’s Wall Street, a huge electronic board continuously updates and displays a rapidly changing figure of American Federal debt, which is almost $38.79 trillion as of 25 February 2026.

This debt is so much higher that if we add the GDP of every country except China, the total figure would still be higher. Every American citizen is under debt of around $113,00-$116,00, and for taxpayers, it is around $277,00 according to data, still increasing every day with an average of 6 billion US dollars.

The continued increase in U.S. government debt constitutes a slow–moving yet impactful threat to the worldwide faith in the U.S. dollar. Though U.S. Treasury securities remain seen as among the safest financial assets, rising debt loads have stoked worries about long-term fiscal sustainability as well as the risk of eroded dollar purchasing power from inflation or depreciation.

1- ECONOMIC SCALE AND STABILITY

The United States has the biggest and most diversified economy in the world, providing depth, liquidity, and resilience to the highest order. High levels of productivity, innovation, and consumer markets all combine to instill confidence in the dollar as a stable store of value. The United States’ economy is estimated at $31.49 trillion as of February 2026 data.

2- WORLD’S RESERVED CURRENCY

The position of the US dollar as a world reserve currency is a function of its extensive use by various actors including governments, central banks, and international organizations for purposes including official reserves, international trade settlement, and financial transactions.

A large volume of international commerce, including major commodities such as oil and gas, is conducted using the dollar; this minimizes costs for participants in these exchanges by reducing costs associated with exchange rate risk. In the financial domain, the dollar is preeminent in international lending and investment, as well as international payment systems, with support from the depth and richness of US capital markets.

Central banks also support these activities through large holdings of dollar-denominated assets, mainly U.S. Department of the Treasury securities, which are valued for their safety, depth, and dependability. These activities cumulatively position the dollar as a core element of the international monetary system.

3- GOLD STANDARD

In 1944, the dollar was fixed to gold at $35 per ounce through the Bretton Woods System, and other global currencies were pegged to the U.S. dollar, making it the world’s main currency. Later, gold convertibility ended due to the United States’ financial difficulties. This did not make the dollar weak — it remained dominant and continues to be powerful today because of the size of the U.S. economy, deep financial markets, and trust in its institutions.

Unlike gold, the dollar earns interest and drives global trade, acting as a modern “gold standard.”

4 – THE PETRODOLLAR

Oil equals dollars. For half a century, that was the “brutal truth” of global finance. Under the petrodollar system, oil-exporting nations agreed to price and sell their crude exclusively in U.S. dollars. This didn’t just help the U.S.; it forced every nation on Earth to hoard greenbacks just to keep their lights on.

But as we move through early 2026, the “exclusivity” of this deal is fading. While the dollar still settles the vast majority of trades, the “monopoly” is over. We are seeing a shift toward a multi-currency energy market:

The Saudi Shift: Saudi Arabia has moved beyond its 1974 “informal” dollar-only pledge. By February 2026, the Kingdom will be actively using the mBridge system to explore non-dollar settlements with major partners like China.

The Rise of Local Settlement: It’s not just about a “rival” currency like the Yuan anymore. It’s about countries like India and the UAE settling trades in Rupees and Dirhams.

The Result: This doesn’t mean the dollar is dead, but it does mean its “forced circulation” is weakening. If nations don’t need dollars to buy oil, they don’t need to hold trillions in U.S. Treasury reserves. That is the real crack in the pillar.

FRIGHTENING INTEREST RATES

Sudden and extreme fluctuations in U.S. interest rates threaten to unravel the dollar’s global dominance. Sharp rate hikes can send borrowing costs soaring, pushing government debt, corporations, and emerging-market borrowers to the brink of default. On the other hand, abrupt rate cuts can devastate returns on dollar assets, triggering a mass exodus of capital toward safer or more profitable alternatives. This relentless volatility risks shaking global financial stability, eroding trust in the dollar, and, if unchecked, could imperil its very role as the backbone of the international monetary system.

TRUST IN AMERICAN LEADERS

Following Russia’s invasion of Ukraine in 2022, the United States, in coordination with allied nations, froze Russian sovereign assets held within U.S. jurisdiction, including an estimated $5 billion in central bank reserves. These sanctions, part of a broader G7 effort, block Russia from accessing or transferring its funds, constraining its financial maneuverability and ability to support military operations.

Although U.S. law traditionally does not allow outright seizure of these reserves, officials have explored the REPO Act (Rebuilding Economic Prosperity and Opportunity for Ukrainians Act) as a framework for using them to aid Ukraine’s reconstruction.

Coupled with freezes on Russian state-affiliated entities and oligarchs, these measures illustrate how the U.S. leverages financial instruments for geopolitical influence while highlighting the legal complexities and risks involved in targeting central bank assets. The action broke the world’s trust on US government and banking systems.

LOSING GLOBAL DOMINANCE

In early 2026, the U.S. dollar is under significant pressure, marking its weakest performance in years amid fears of de-dollarization, aggressive tariff policies, and high federal debt. Continued tariffs have pushed the dollar to four-year lows, casting the U.S. as a driver of deglobalization, while high debt-to-GDP ratios and declining investor confidence signal a potential long-term erosion of its global dominance. Pressure on the Federal Reserve to cut interest rates further threatens the currency, with a weaker dollar raising import costs and complicating debt repayment.

IMPACT OF DE-DOLLARIZATION

De-dollarization, the global move away from the U.S. dollar in trade, finance, and reserves, is emerging as a serious challenge to America’s financial dominance. As countries diversify into alternative currencies and regional payment systems, demand for the dollar is under pressure, weakening its exchange rate and increasing volatility. Over time, this shift could raise borrowing costs, erode the dollar’s safe-haven appeal, and diminish U.S. influence in global finance, signaling a potential long-term recalibration of the international monetary order.

HOW BRICS NATIONS CHALLENGING US DOLLAR

The ascent of BRICS represents an increasing threat to the U.S. dollar’s global supremacy. By encouraging trade in their own currencies, establishing alternative payment networks, and coordinating reserves via the New Development Bank, member nations—particularly China and Russia—are actively reducing dependence on the dollar. If sustained, these initiatives could gradually undermine the dollar’s reserve currency status, decrease global demand, and diminish U.S. influence in international trade and financial systems.

CONCLUSIONS

Despite mounting challenges such as rising U.S. debt, inflationary pressures, and the gradual de-dollarization efforts led by emerging economies and blocs like BRICS, the dollar continues to be the dominant currency in global reserves. There is currently no single, credible alternative capable of matching the dollar’s liquidity, depth, and global acceptance across trade, finance, and reserves.

As a result, the dollar is not on the verge of an immediate collapse; instead, it is experiencing a more gradual, long-term transformation in its role. This “slow burn” decline reflects structural shifts in the international monetary system, where global reliance on the dollar may steadily decrease as countries diversify holdings, develop alternative payment systems, and engage in trade using non-dollar currencies. While the dollar remains central to global finance, these trends highlight the potential erosion of its hegemonic influence over time, signaling a period of strategic recalibration for both the United States and the broader international economic order.

Relevant Topics: